A Biased View of Wyhy

Table of ContentsFacts About Wyhy UncoveredFacts About Wyhy UncoveredWhat Does Wyhy Do?3 Easy Facts About Wyhy DescribedGet This Report on WyhyGetting The Wyhy To Work

Several lenders desire to see a DTI of no more than 36% and so yours fits within this guideline. With the very same quantity of debt yet an income of $5,500 a month, the DTI is 39.7%, and if a lender calls for one of no even more than 36%, you might require to put down more cash or pay off some financial obligation prior to you certify.As an example, allow's claim that you're simply over the DTI limit, yet the lending institution wants it addressed prior to approving your finance. In our example, you have a personal loan with a high settlement and a remaining balance of $3,000. You could experiment to see if you might make a reduced deposit and use those funds to repay the individual funding.

Wyhy Fundamentals Explained

The number given by each of them is likely to be similar yet not necessarily identical. The 3 primary firms that check a consumer's credit scores and give ratings for lending institutions are Experian, Equifax, and TransUnion. You can inspect your credit rating reports from each of these 3 companies (not your ratings however the records) annually completely free.

Also, inspect your credit score reports to make sure there aren't any type of mistakes that can be damaging your credit rating, and reach out to the firms to make any modifications. This is additionally a great possibility to look for any type of signs of identity theft. If you see anything dubious or inaccurate, addressing that issue can aid to clear any kind of dings on your credit scores.

All About Wyhy

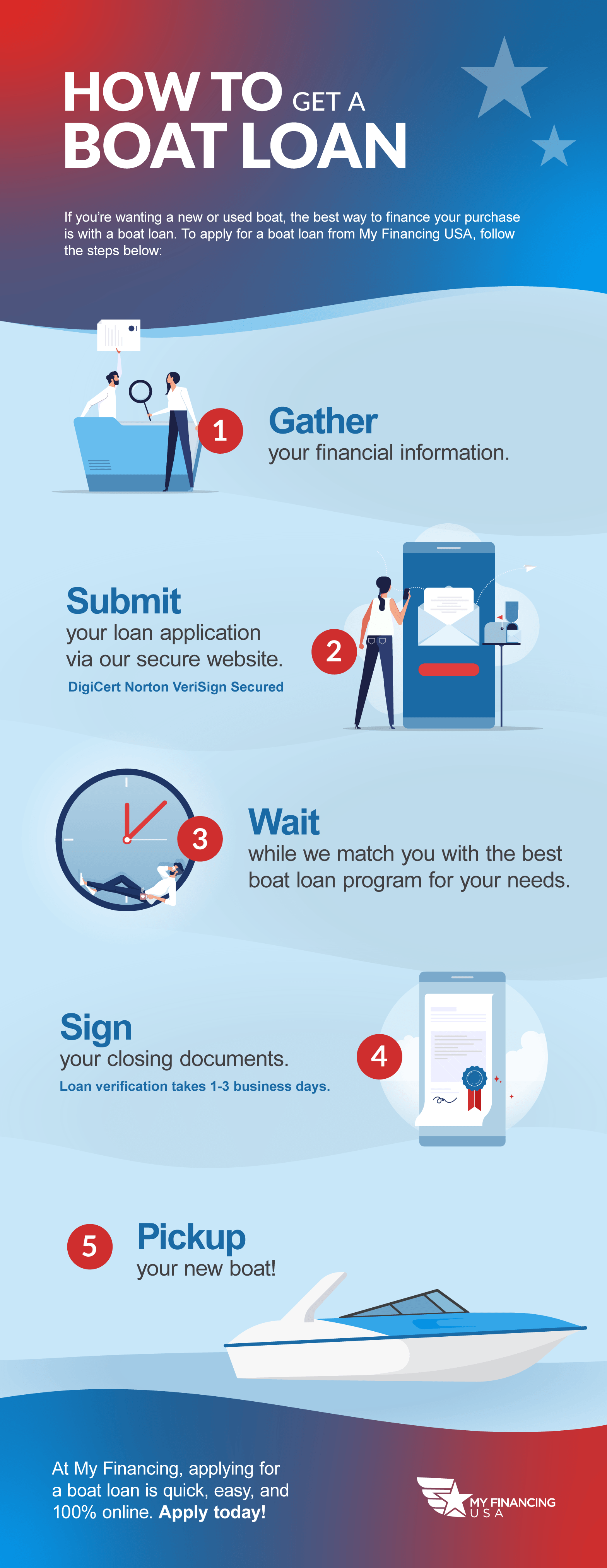

At SCCU, this procedure can be completed in as little as five minutes. When you're exploring financial organizations and their watercraft finances, ask pals and household participants who have watercrafts where they obtained their funding and ask about their experiences with their lenders.

Equipped with the understanding of what lending institutions normally look for in watercraft car loan candidates such as DTIs and credit report ratings you can contrast the monetary organizations on your listing to locate the one that uses what you need. credit union in wyoming. The rate of interest rate is a portion that the lending institution will certainly charge you on your boat financing, and as your primary balance goes down, the quantity of your repayment that mosts likely to rate of interest will likewise drop

Not known Facts About Wyhy

Regarding funding kinds, taken care of price financings are the most basic, and for several customers, more effective. With this type of financing, the principal and interest repayment stays the same for the useful content life of the financing, that makes it the simplest to budget, and you don't have to stress over the rates of interest rising in the middle of the financing.

It's feasible with a variable price lending that the rate of interest can go up or down. During times when rates of interest on watercraft financings are already reduced (such as in 2021), it's not as likely to drop much further. Sometimes, a funding is established up as a balloon payment car loan, one in which settlements might resemble a taken care of or variable car loan, yet the whole balance is due after a reasonably short time possibly after two or three years.

10 Simple Techniques For Wyhy

Contrasting the APR amongst loan providers, additionally examine to see how much of a gap there is between the interest rate and APR at each one. The higher the difference, the extra fees the monetary organization is billing on their boat car loans. https://disqus.com/by/disqus_dwcms9sX7l/about/. Different lending institutions require various portions of down settlements with 10% or 20% being one of the most typical

When a lending institution details a down settlement demand, note that this is the minimum that's needed you can make a larger one to get a smaller lending. The down repayment and the DTI are intricately connected. A consumer might not qualify for a watercraft loan without a down repayment being made or with just a small one.

See This Report about Wyhy

So, as you look for a financing, you can explore various deposit total up to see what is most economically practical for you and what placements your DTI most successfully (credit union in wyoming). Learn the maximum lending term that a lender supplies, which can be revealed as a number of months or years

The longer the term that you pick, the smaller sized your financing settlement. A longer term can provide you with a payment that fits much more conveniently into your spending plan. That stated, the shorter the term, the less passion you'll repay over the life of the financing, so factor in both considerations as you select your term.

If so, ask your loan provider if there are any kind of fines related to paying the lending off faster (prepayment penalties). If there aren't, when you have extra money, you might place the cash down on the watercraft finance to pay it off extra swiftly and pay much less interest overall - https://wyhy82003.blog.ss-blog.jp/2024-04-24?1713957646. Each lender can determine what to charge, and charges can therefore vary dramatically amongst banks